by Garrett Fisher

April 13, 2014

Obviously, I spend a lot of time talking about economic innovation and it has become evident that not all interpretations of economic innovation are the same. Most, when hearing the phrase, would think that it relates to a more productive and efficient economy and that said efficiency and productivity is inherent progress and good for society. In the short term, that is the case. In the long-term, we speed up the rat race and many of those new efficiencies are factored into new market pricing and the struggle for the average person to survive economically remains the same. Economic innovation, in my definition, is far more innovative than that.

A worthy question is: where does economics come from? If you’re not stumped by the question, then a common response would be “the government” or “the rich.” Thinking for a minute about the basics of current economics, supply and demand, who controls demand? Does not the most average of economic participants control demand: you, me, and most everyone else? When we demand something, prices go up initially, and more suppliers are attracted into the market and, in theory, the price comes back down. Higher capitalized businesses and individuals generally have the capital to be suppliers or control them; yet, who is controlling the suppliers? Those with demand for a product or service. Therefore, one can realistically understand that population, sheer mass, drives the economy.

So, then, does the economy come from the masses? That’s not an exact answer. Why do the masses purchase what they do, anyway? Where does that come from? The answer is how each person thinks is where the economy comes from. How we think drives what we decide we need and want, and that drives what we spend our money on. How we collectively spend our money creates a system, and that system gets regulated and morphs into the economy that we know.

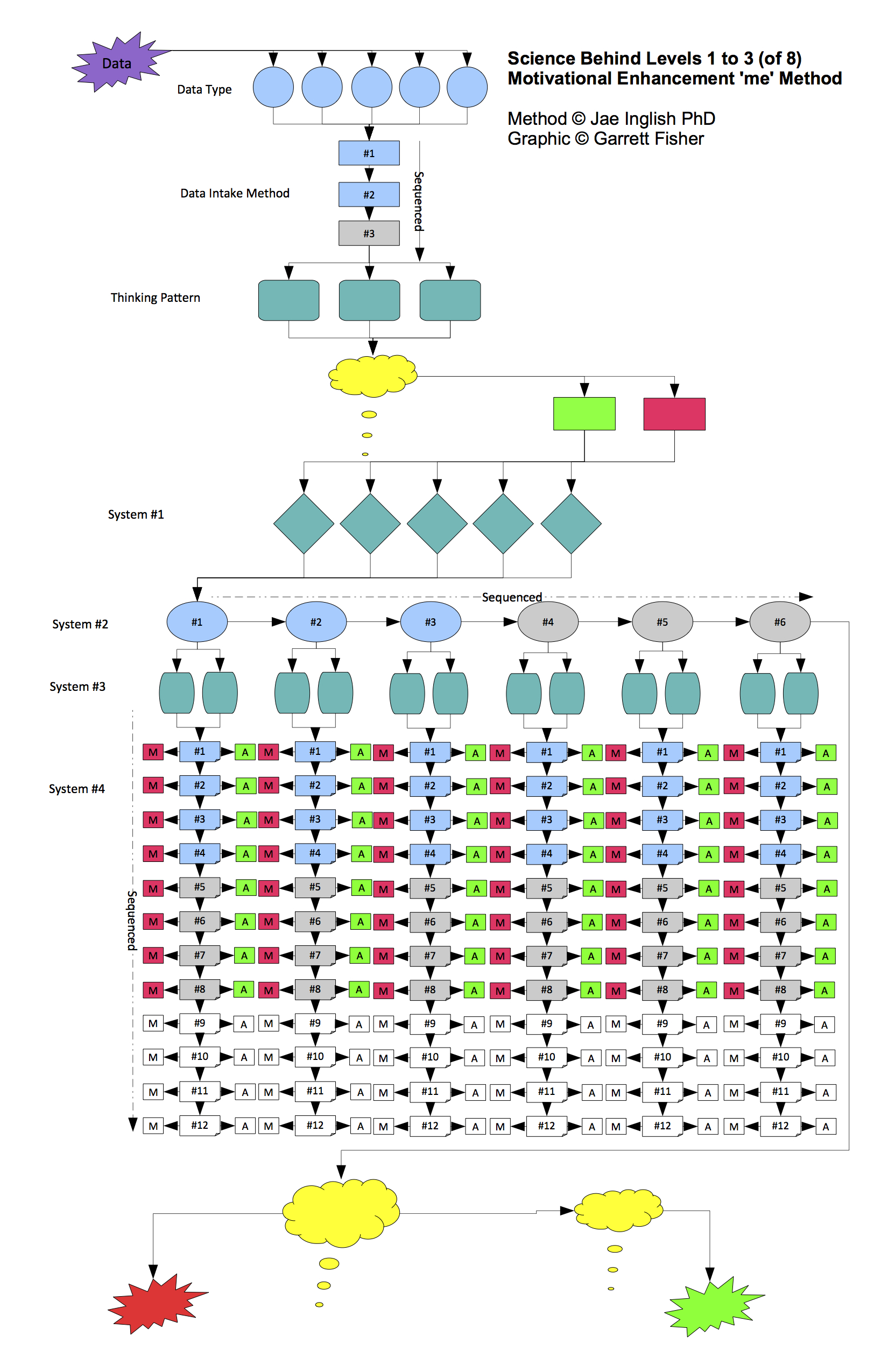

Thinking is not a random proposition. Science tells us that, while humans are individuals and unique, there are classification systems to how we think, learn, and what we are pursuing. Therefore, if we can apply those classification systems in the mind to the broader economy, we can, in effect, close the loop on the entire system. Instead of trial and error monetary and tax policy about what “will work,” this new definition of economic innovation goes to the root of what causes the challenges and trials that we face and, instead of messy debate and dislocating economic changes, the study of economics can be connected to the very sources of whether it will work or not. Note the following chart (taken from my book, The Human Theory of Everything):

This diagram represents some of the known classification systems available to science. A person is effectively born with a preference for one or more of each of the available systems. When factoring the probability of individuals being the same in all respects, it is statistically impossible to have two people be the same; yet, we can understand profound commonalities. Imagine the power the translating these characteristics to the economy as a whole.

In a separate article, I have articulated that our current economy is tied to Stone Age thinking and that we are a fear dominated society out of concern for basic needs being met. Economic innovation stands to break an economy out of that cycle and have the discussion be much larger than the common arguments of the day. Humans do not want to sit in smoggy traffic, work in cubicles, and gain weight due to the stress of working with antagonistic coworkers. We all have passions and desires to pursue any number of enlightened fields and yet we don’t even begin to follow those because the need to eat predicates a need to be economically miserable working at displeasing jobs. Granted, some do like their employment; however, most have dissatisfaction.

Fear has created a miserable economy. With a miserable economy, how can the human race produce positive things that create an enjoyable existence? It makes little sense that it would, and evidence shows that it does not. To truly innovate in this economic sense would be to step out of the cycle of fear over basic needs and engineer a solution that takes into account who we are as people and finds a negotiated answer where needs get met across the population. In effect, it is a mix of motivation, sociology, finance, and economics – something few, if any, have done. That is the definition of economic innovation that I am speaking of.